quant.ly labs · research note 001

Buffett's Million-Dollar Bet: What It Actually Proved

Key takeaways

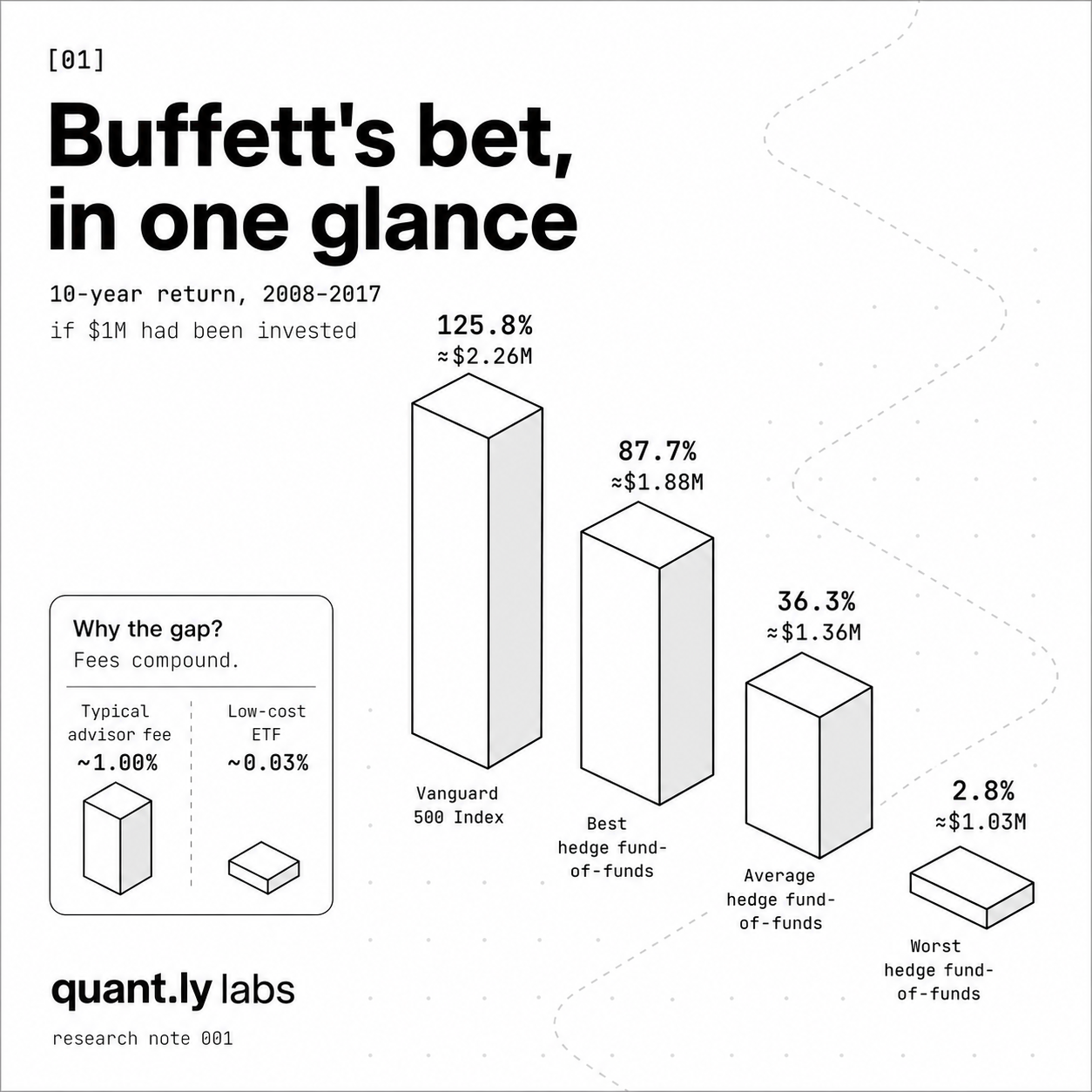

- In 2007, Warren Buffett bet $1 million that a single S&P 500 index fund would beat five funds-of-hedge-funds over ten years. The Vanguard fund returned 125.8%. The average hedge fund-of-funds returned 36.3%.

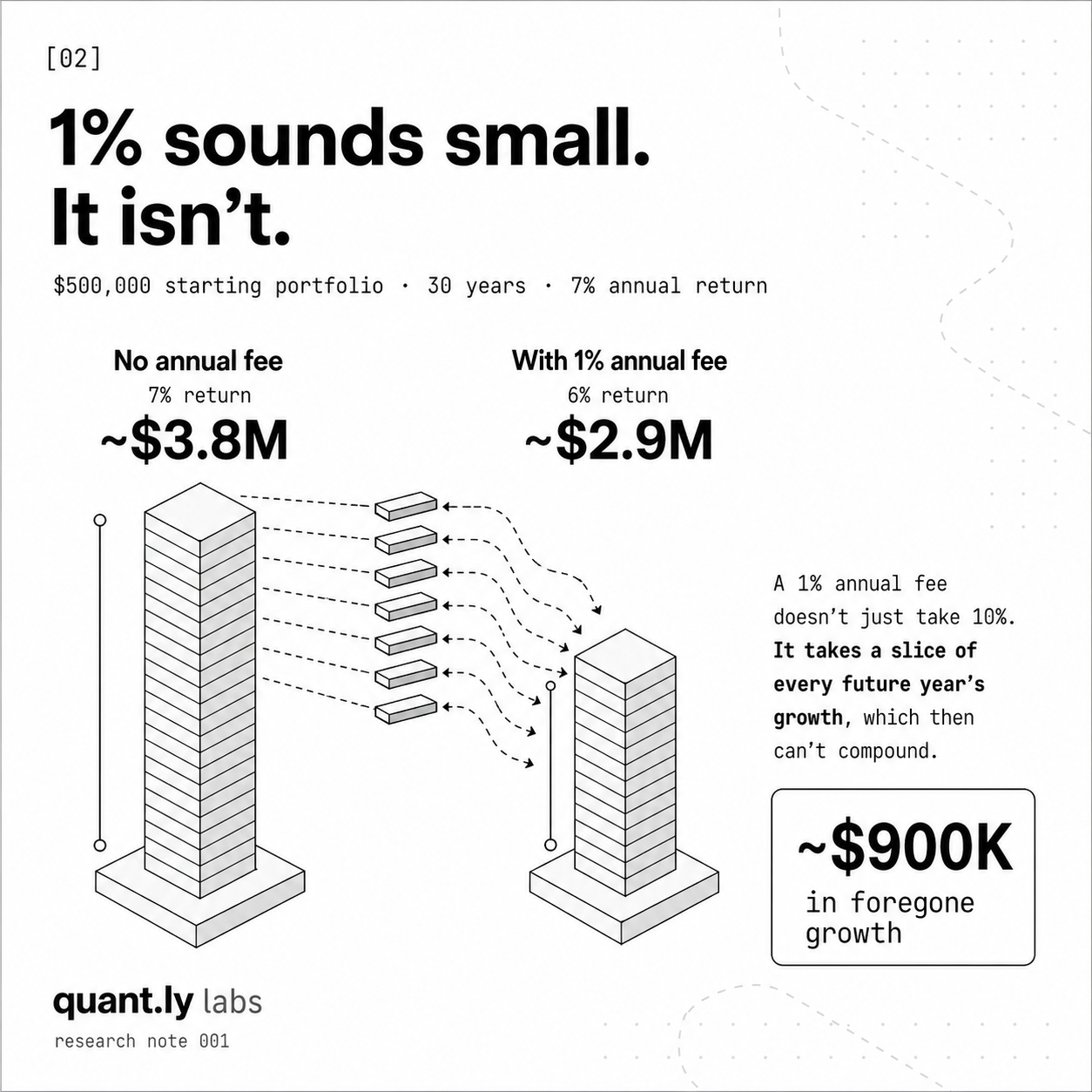

- The deeper lesson is structural: 1% annual fees compound backwards. On a $500,000 portfolio at 7% returns over 30 years, a 1% fee costs about $900,000 in foregone growth.

- Modern advisors mostly assign clients to pre-built model portfolios kept in line by rebalancing software (Orion, iRebal, AdvisorEngine, Nitrogen). The strategic call (how aggressive your allocation is) is what costs more than the fees.

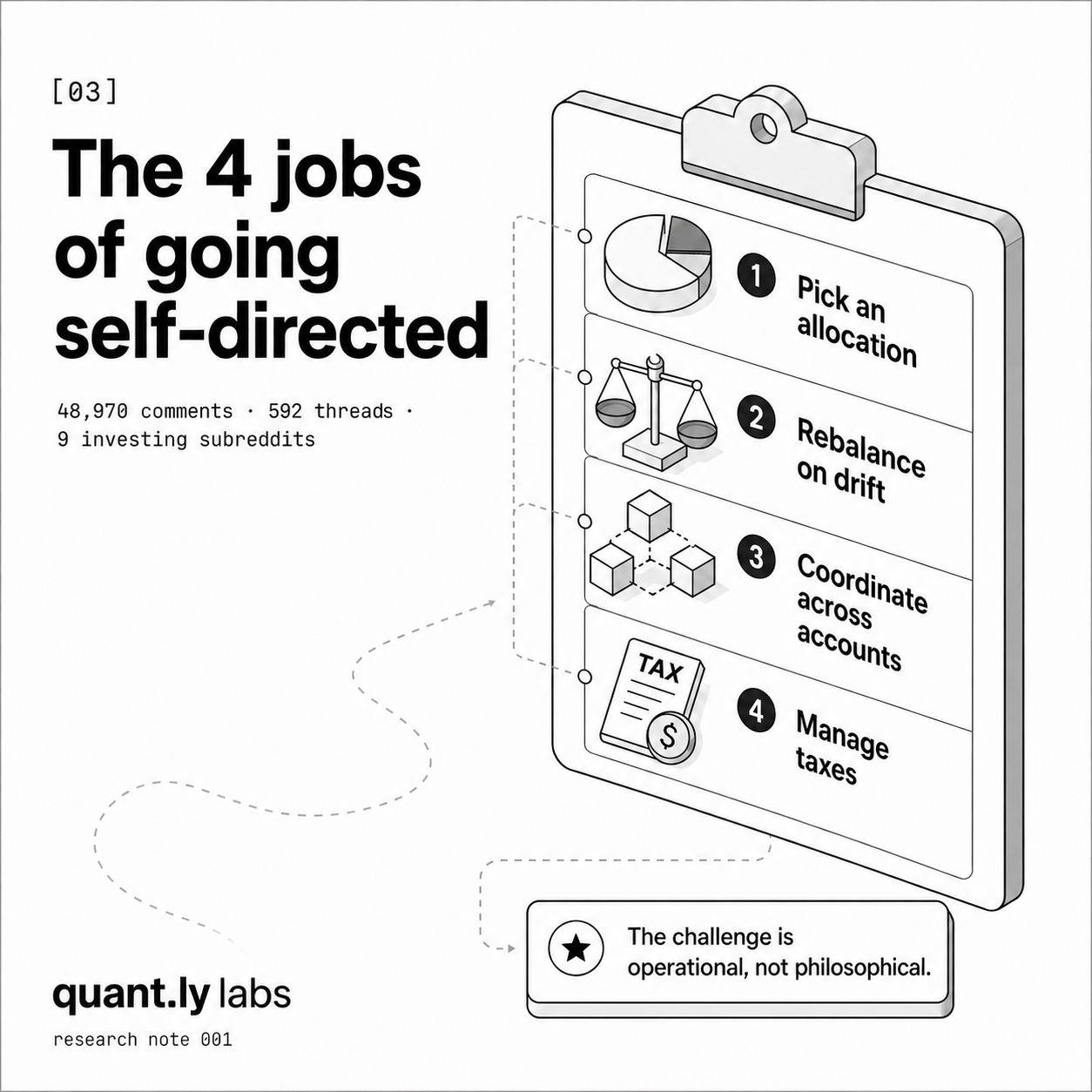

- quant.ly Labs analyzed 48,970 comments across 592 threads from nine investing subreddits. Self-directed investors converge on four operational tasks: pick an allocation, rebalance on drift, coordinate across accounts, manage taxes.

- The operational gap, not the philosophy, is where most self-directed investors fail.

In 2007, Warren Buffett bet $1 million that a single index fund would beat five hand-picked hedge funds over the next decade. He won. The lesson most people pull from that story is the wrong one.

The bet

The setup was clean. Buffett picked the Vanguard 500 Index Admiral, a low-cost fund that buys the S&P 500 and does nothing else. Ted Seides, then a managing director at Protégé Partners, picked five funds-of-hedge-funds. These pool money across multiple hedge funds run by people whose entire job is to beat the market. Stakes: a million dollars to charity. Ten-year horizon. Public scoreboard.

Most reasonable people thought Buffett was overconfident. Hedge funds have every tool. Short selling, leverage, derivatives, currency arbitrage. They’re run by people paid to pay attention all day. An index fund just sits there. Surely the pros would win.

The numbers

Who won? Buffett, by a landslide.

How much? The Vanguard fund returned 125.8% over the decade. The average return across Seides’s five hedge fund-of-funds: 36.3%. The best of the five: 87.7%. The worst: 2.8%.

Was it close? Not at first. The 2008 crash dropped the S&P fund 37% in year one. That put it roughly 13 points behind the hedge funds going into year two. The index clawed back through 2009 and 2010, but Buffett was still losing the bet at the end of year three. The crossover didn’t happen until around 2012 or 2013. By year seven the index was running away. Seides conceded before the clock ran out. The real lesson of the bet isn’t that index funds win fast. It’s that index funds win if you don’t blink.

Was it a fluke? Standard & Poor’s publishes the SPIVA Scorecard twice a year. It tracks how active managers do against their benchmarks over rolling periods. The honest summary across decades of data: most active managers lose to their benchmark over ten or more years. The hedge funds in Buffett’s bet weren’t outliers. They were typical.

The real lesson

The popular reading is “index funds beat hedge funds.” True, but small. The bigger lesson is structural: fees compound. And they compound backwards.

A 1% annual fee doesn’t cost you 10% over ten years. It costs you a slice of every future year’s growth, which then can’t compound. Run the math on a $500,000 portfolio at 7% annual returns over 30 years. Without fees, it grows to roughly $3.8 million. Add 1% in annual fees. Your effective return drops from 7% to 6%. Now it grows to about $2.9 million. The fee took $900,000 off your retirement, not $150,000.

Hedge funds were the extreme case: 2% annual fees plus 20% of profits. That structure is mathematically incompatible with beating the market over time. Buffett didn’t need his bet to play out. He just had patience.

Why this matters today

Your advisor probably isn’t running a hedge fund. They’re more likely doing this. You fill out a risk-tolerance questionnaire. They assign you to one of five or ten model portfolios their firm maintains. Rebalancing software keeps your account aligned with that model. Cerulli’s most recent research shows roughly 22% of advisor practices identify as model-portfolio users, with adoption higher at large RIAs and forecast to grow. The “stewardship” you’re paying for is, in operational terms, a software service.

For that service you typically pay 1% of your assets per year. On a $500,000 portfolio, that’s $5,000 every year. Roughly $416 a month. The math from above still applies: at 7% returns over 30 years, that 1% costs you about $900,000 in foregone growth. You’re paying for a model portfolio with the income from a small house.

This isn’t a hit on advisors. Vanguard’s own “Advisor’s Alpha” research finds that good advisors add roughly 3% in value per year. But the bulk of that value comes from behavioral coaching (stopping you from selling at the bottom in March 2020), tax planning, estate coordination, and insurance review. Not from managing your portfolio. The portfolio management is the part the software does. Whether the rest of the bundle is worth 1% of your wealth every year is a question you should get to ask, not have decided for you.

Buffett, in his 2017 letter to shareholders, put it plainer than anyone:

“When trillions of dollars are managed by Wall Streeters charging high fees, it will usually be the managers who reap outsized profits, not the clients.”

That’s not a takedown of any individual person. It’s a statement about how the math works when fees scale with assets. If your advisor’s compensation grows automatically when your portfolio grows, independent of whether they did anything to grow it, you’re paying for outcomes the software produced.

A confession

I’ll come clean. I paid an advisor 1% of my assets for ten years. The starting capital came from a windfall. Stock options that vested in a company IPO. Hiring someone seemed like the responsible thing to do with money I had no instinct for.

Over those ten years, after fees, the portfolio gained roughly 2% per year.

Then I kick myself. The simplest version of what I should have done was something my father literally said to me. “Just put it in an S&P 500 index fund.” I didn’t listen.

He retired 28 years ago with a modest amount and still has a sizable portion of it left. He’s done it himself the whole time. No advisor. No fees. Index funds, mostly.

Here’s the cost of not listening, on a clean $500,000 illustrative basis over the same decade my advisor managed my windfall (2013–2022):

| Annual return | $500K becomes | 10-year gain | |

|---|---|---|---|

| With my advisor | 2.0% (after fees) | $609,497 | ~$110,000 |

| What my father said to do (S&P 500) | 12.5% | $1,633,550 | ~$1,133,000 |

| Difference | ~$1,024,000 |

S&P 500 figures use annual total returns 2013–2022, dividends reinvested.

What did I get from my advisor for the gap? A holiday gift basket. A nice one.

I want to be fair about the rest. He wasn’t a passive button-pusher. He worked with my tax guy. He coordinated lot selection on the harvests. He sold the right shares at the right times. He was available for as many meetings as I wanted. I just rarely took him up on more than a couple a year. The standard “they don’t really do anything” line isn’t fair to him.

This is where he failed me, and where the structural critique still lands. He let me stay too conservative for my age and risk tolerance. More cash, more bonds, less equity than the math wanted for someone with decades of horizon. That call wasn’t operational. It was strategic. The 2% return after fees isn’t because the execution was bad. It’s because the strategic posture was wrong, never got challenged, and quietly cost more than the AUM fee did.

That’s the structural point. The bundle isn’t empty. The execution layer can be perfectly competent. The strategic call sits between you and someone whose incentives don’t always line up with yours. My advisor’s compensation grew the same whether my portfolio was 80% stocks or 80% bonds. Mine didn’t.

What self-directed investors actually do

For this research note, quant.ly Labs analyzed 48,970 comments across 592 threads from nine investing subreddits: r/Bogleheads, r/financialindependence, r/fatFIRE, r/personalfinance, r/dividends, r/investing, r/leanFIRE, r/stocks, plus the long-form Bogleheads forum. Here’s what comes up, ranked by engagement.

Methodology: comments scraped from public Reddit JSON endpoints in March 2026. “Mention” counts are case-insensitive substring matches across comment bodies. Each comment is counted once regardless of author. Topic counts use a curated keyword set per topic (e.g., “rebalanc” for the rebalancing topic) and are deduped at the comment level.*

Top topics, by comment count:

| Topic | Comments | Where it dominates |

|---|---|---|

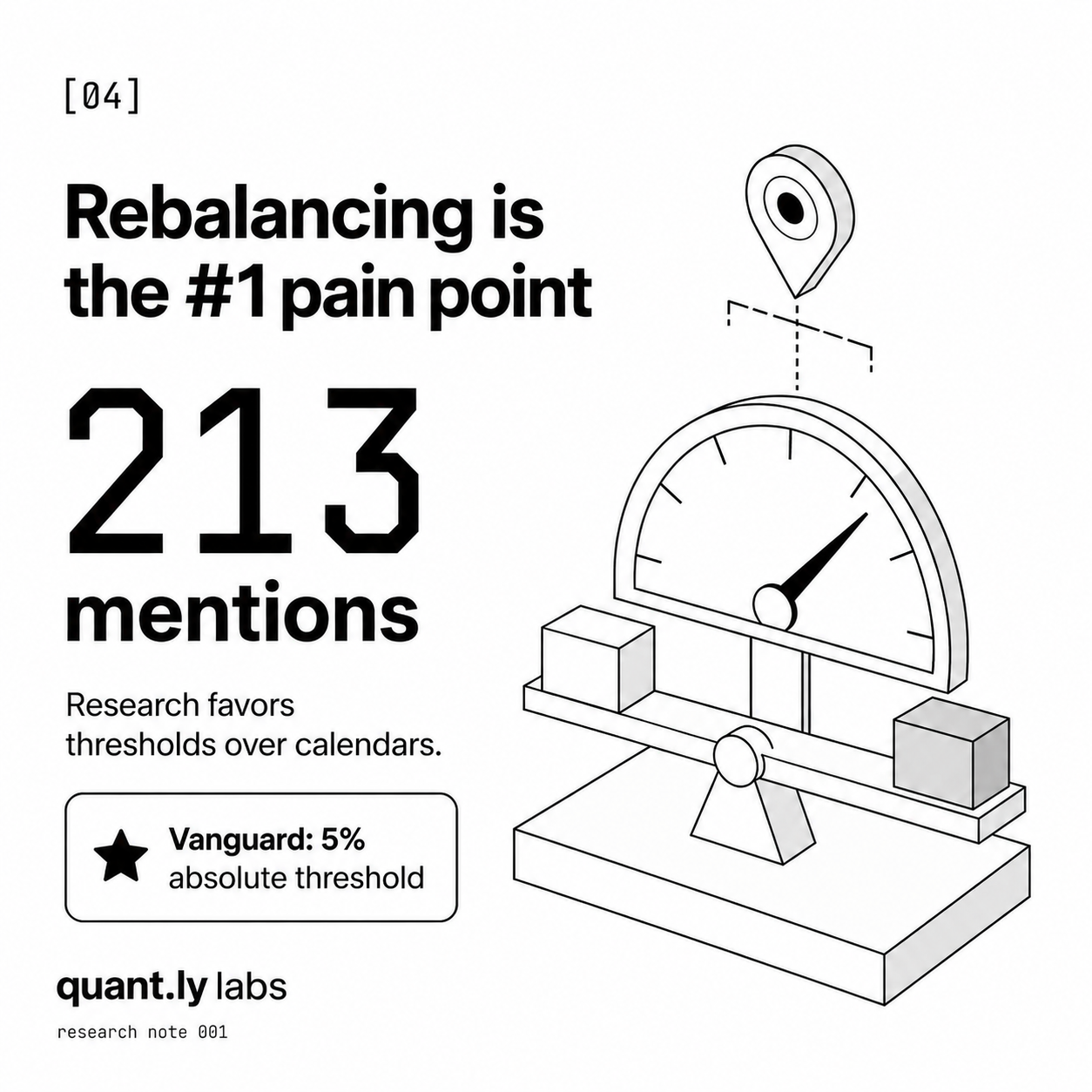

| Rebalancing | 213 | r/Bogleheads, r/financialindependence |

| Roth conversions | 170 | r/financialindependence, r/fatFIRE |

| Tax-loss harvesting | 103 | r/Bogleheads, r/fatFIRE |

What they reach for instead of an advisor:

| Tool category | Mentions | Recurring sentiment |

|---|---|---|

| Brokerage built-in tools (Vanguard, Fidelity, Schwab) | 1,207 | ”Broken” comes up a lot |

| Spreadsheets / Excel | 714 | Works, until accounts pile up |

| Human advisors | 322 | Often as foil (“I left mine”) |

| Aggregators (Empower, Quicken, Mint legacy) | 227 | Mostly negative (“every tool fails eventually”) |

What’s not on this list: picking stocks

Worth surfacing because it’s the question most people raise first. Across the 48,970 comments, individual stock-picking is a minority activity. The dominant pattern is what my father said. Index funds, low cost, set the allocation, leave it alone.

- The “active stock-picker” cluster (r/stocks + r/investing, what the dataset tags as “Curious Tinkerers”) shows up as 14 threads / 150 comments, about 0.3% of the dataset

- Even that cluster self-describes as “90% index, 10% fun money.” The bulk is still indexed. Individual stocks are a small side bet.

- The Bogleheads philosophy (134 threads, 2,308 comments, the largest single-community presence in the dataset) is explicit: don’t pick stocks. Don’t time the market. Buy the whole market through low-cost index funds and let compounding do the work.

Self-directed doesn’t mean active. For most people in this data, it means: I make the structural decisions (what to own, how much), and let the market do the rest.

The four-task playbook

Across the dataset, four tasks repeat. The other things people talk about (fund-pair selection, glide-path optimization, tactical tilts) show up in single-digit thread counts. These are the four things people actually have to do.

| # | Task | Why it matters | Where it breaks today |

|---|---|---|---|

| 1 | Pick a target allocation | The yardstick everything else measures against | Self-directed brokerages won’t propose one on their non-managed surfaces. Robo-advisors will, for a fee. Forum templates are the third path. |

| 2 | Rebalance when you drift | Risk control plus a buy-low-sell-high discipline | Traditional brokerages don’t send drift alerts on accounts you self-manage. Robos do, for the accounts they manage. Tax-aware execution across accounts is hard math (which account, which lots). |

| 3 | Coordinate across accounts | Your real risk lives in the combined view | Some brokerages import external accounts but want you to move money to them. Aggregators break. Spreadsheets fall apart at three accounts. |

| 4 | Manage your tax bill | Bracket arbitrage. One of the biggest drags on long-term returns. | Wash-sale rule is invisible across accounts the tool doesn’t see. Bracket and conversion math has standalone tools (Boldin, Pralana, ProjectionLab), but none integrated with where your assets actually live. |

Each one gets the same five-question treatment below. We’re not telling you what to do. We’re telling you what people who do this do, what they struggle with, and what a better tool would look like.

1. Pick a target allocation

What it is. Your target allocation is the mix you want your portfolio to hold. For example, 70% in stock index funds and 30% in bond funds. It’s a statement of how much risk you’re willing to live with.

Why do it. Without a target, there’s no yardstick. You can’t know whether your portfolio is doing what you wanted, or how far it’s drifted from what you wanted, if you never said what “right” looks like.

The challenge with the tools available. Two paths exist. Neither is great. Traditional self-directed brokerages (Vanguard, Fidelity, Schwab on their non-managed sides) won’t propose an allocation. That would cross the legal line into giving personalized advice. The robo-advisors (Betterment, Wealthfront, Schwab Intelligent Portfolios, Vanguard Digital Advisor, Fidelity Go) will. They map you to one of a small number of pre-built model portfolios for a recurring fee. That’s a cheaper, automated version of what a 1% advisor does. If you want to truly self-direct without paying anyone, you’re picking from forum-tested templates.

What people end up doing today. Two patterns dominate. Pick a target-date fund (a single fund that automatically adjusts the stock-to-bond ratio as you get older) and let that be the target. Or pick a three-fund split (a US stock index, an international stock index, a bond fund) at a ratio they read about on a forum. From a 47-thread sub-analysis on this question, the dominant advice was: “Pick a sensible default and move on. The difference between 60/40 and 70/30 is dwarfed by your savings rate.”

What would be ideal. A surface that proposes a starting allocation based on your age, your existing accounts, and your goals. Explains why it picked that. Lets you edit it freely. Without ever telling you what you must do.

2. Rebalance when you drift

What it is. Over time, the parts of your portfolio that grow fastest (usually stocks) become a larger share of the total than you intended. Rebalancing means trimming what’s grown and adding to what hasn’t, to bring the mix back to your target.

Why do it. A portfolio that’s drifted too far carries more risk than you signed up for. Rebalancing is risk control. It also forces a “trim what’s expensive, add to what’s cheap” discipline that’s much harder to do by gut feel.

The challenge with the tools available. Rebalancing isn’t just a question of when. It’s a question of how you do it without creating a tax bill. Selling appreciated stock funds in a taxable account triggers capital gains taxes that can wipe out the value of the rebalance. The tax-aware version of the question, “should I sell from my taxable account or my IRA, and which specific lots?”, is genuinely hard math. The research is clear that threshold-based rebalancing outperforms calendar-based rebalancing on risk-adjusted return. Vanguard’s 2015 “Best Practices for Portfolio Rebalancing” paper recommends a 5% absolute threshold. Daryanani’s 2008 Journal of Financial Planning paper “Opportunistic Rebalancing” recommends a 20% relative threshold. Both beat fixed quarterly schedules. But you need both the monitoring (traditional brokerages don’t send drift alerts on accounts you self-manage; robo-advisors do for the accounts they manage) and the tax-aware execution across all your accounts (which almost no retail tool handles end-to-end) to get there.

What people end up doing today. The clever workaround that comes up repeatedly in the data: rebalance with new money. Redirect your next deposit to whatever’s underweight. No selling, no taxes. 8 of 47 drift threads celebrate this as a breakthrough. For everything else, it’s a calendar reminder and a manual check. Rebalancing came up 213 times in the dataset, the single most-discussed topic. Most of those are someone asking “is it time yet?” with no clean way to answer.

What would be ideal. An always-on view of where your portfolio sits relative to its target, with a clear signal when you’ve drifted past your tolerance band. Plus a tax-aware “here’s the cheapest way to fix it” calculation that knows which account to use and which lots to sell.

3. Coordinate across accounts

What it is. Most people don’t have one investment account. They have several. A workplace retirement plan (a 401(k) or 403(b)). One or two individual retirement accounts (a Roth IRA, a traditional IRA). Often a regular taxable brokerage account. Sometimes a spouse’s accounts on top. For allocation purposes, all of these are one portfolio.

Why do it. If you only look at each account by itself, you miss the full picture. Your 401(k) might be 100% stocks. Your Roth IRA might be all bonds. Your taxable account might be tilted toward international. Looking at any one in isolation tells you nothing about your real risk. Only the combined view does.

The challenge with the tools available. Some major brokerages (Morgan Stanley, Schwab, Fidelity Full View) do let you import external accounts. The motive is rarely neutral. The pitch is “see everything in one place.” The offer underneath is “now move it all to us.” The third-party aggregator category that’s supposed to be neutral on consolidation (Empower, Quicken, Mint while it lived, Personal Capital) got 227 mostly-negative mentions in the dataset. The recurring complaint from veteran self-directed investors: “every tool fails eventually.” Connections drop. Joint accounts get misclassified. Account types get read wrong. Accuracy degrades over time.

What people end up doing today. A spreadsheet. Manually updated. The phrase “spreadsheet” or “Excel” came up 714 times in the dataset, second only to brokerage tools at 1,207 mentions of “what I use.” A spreadsheet works fine at one or two accounts. It falls apart at three or more.

![]()

What would be ideal. A read-only view that connects to every account you have, has no incentive to consolidate them at any particular firm, shows the household-level allocation in one picture, and stays accurate without you having to maintain it.

4. Manage your tax bill

What it is. Tax management for self-directed investors comes down to three connected skills.

- Tax-loss harvesting in taxable accounts only. Sell positions at a loss, claim the loss, immediately buy a similar (but not identical) fund so you stay invested.

- Bracket awareness. Pay attention to the tax bracket cliffs (15% vs 20% long-term capital gains, the Net Investment Income Tax threshold at $200,000 single / $250,000 married, Medicare premium surcharges in retirement) and time realized gains and losses to stay below them.

- Roth conversion planning. Move money from a traditional IRA to a Roth IRA in years when your income is low. Pay tax now at a known rate to avoid a possibly higher one later.

Why do it. Taxes are one of the biggest drags on long-term returns. The numbers are real. A high earner who realized $100,000 in capital gains and harvested $50,000 in losses against them stays in a lower bracket and saves thousands of dollars. A retiree who converts $30,000 from a traditional IRA to a Roth in a low-income year before Social Security kicks in can save five figures over a decade.

A note on retirement accounts. Tax-loss harvesting itself only applies to taxable accounts. Retirement accounts (401(k), traditional IRA, Roth IRA) grow tax-sheltered while the money is inside. With a traditional IRA you pay tax on the way out at retirement. With a Roth you don’t. That’s why withdrawal sequencing and Roth conversion timing are the adjacent skills. Together these three made up the dominant tax conversation in the data: 103 mentions of tax-loss harvesting plus 170 of Roth conversions.

The challenge with the tools available. The wash-sale rule is the showstopper for harvesting. A rule in the US tax code (section 1091) says you can’t claim the loss if you buy a “substantially identical” security within 30 days of the sale, in any of your accounts, including your spouse’s IRA. If the wash sale lands inside a retirement account, IRS Revenue Ruling 2008-5 makes the disallowance permanent. The loss is gone, not deferred.

Every major automated tax-loss-harvesting product (Wealthfront, Betterment, Schwab, Fidelity) explicitly disclaims monitoring this across accounts they don’t custody. The bracket and Roth conversion questions are even harder. They require modeling your projected income, your realized gains so far this year, your bracket cliffs, and any pending major events (selling a house, taking a bonus, retiring) all together. Standalone planning tools (Boldin, Pralana, ProjectionLab) model this in detail and FIRE communities run multi-thread comparisons of how each handles 32% bracket fills, IRMAA tiers, and ACA cliffs. None of them are integrated with where your assets actually live.

Every major automated tax-loss-harvesting product (Wealthfront, Betterment, Schwab, Fidelity) explicitly disclaims monitoring this across accounts they don’t custody. The bracket and Roth conversion questions are even harder. They require modeling your projected income, your realized gains so far this year, your bracket cliffs, and any pending major events (selling a house, taking a bonus, retiring) all together. Standalone planning tools (Boldin, Pralana, ProjectionLab) model this in detail and FIRE communities run multi-thread comparisons of how each handles 32% bracket fills, IRMAA tiers, and ACA cliffs. None of them are integrated with where your assets actually live.

What people end up doing today. Most people skip tax-loss harvesting entirely. The minority who try do it manually and hope they didn’t trigger a wash sale somewhere. Bracket awareness for most retail investors comes once a year, at tax time, when it’s too late to do much about it. Roth conversion conversations dominate the FIRE communities precisely because there’s no tool integrated with where the assets live. People bounce between a planning tool, a spreadsheet, and a CPA call.

What would be ideal. A view that shows every harvest opportunity across all your accounts at once, models the bracket math (your projected income, your gains so far, your bracket thresholds), flags wash-sale risk before you commit, helps you pick partner funds that aren’t substantially identical, and projects forward to show whether a Roth conversion this year would save money over the next decade.

The honest read

The philosophy is well-documented. The math favors it. The operations are where it breaks down.

People don’t fail because they don’t know what to do. They fail because the tooling forces them into spreadsheets that fall apart at three accounts, or into automated tools that go blind the moment a transaction crosses a custody boundary.

Where we come in

That operational gap is what we’re working on. quant.ly is read-only. We connect to the brokerage accounts you already have, show you the household-level view across all of them, and model what a move would do (to your allocation, to your taxes, to your wash-sale exposure) before you make it. We don’t move money. We don’t take custody. You decide. We measure.

If that sounds useful, join the waitlist.

This is Research Note 001 from quant.ly Labs. We publish what we learn from synthesizing self-directed investor conversations. Currently across r/Bogleheads, r/financialindependence, r/fatFIRE, r/personalfinance, and the long-form Bogleheads forum. Read-only data, opinion-free synthesis. We share what people do, what they struggle with, and what the math says.

Frequently asked questions

- What did Warren Buffett's million-dollar bet prove?

- In 2007, Buffett bet $1 million that a Vanguard S&P 500 index fund would beat five funds-of-hedge-funds picked by Ted Seides at Protégé Partners over a decade. The Vanguard fund returned 125.8%. The average return across the five hedge fund-of-funds was 36.3%. The deeper lesson isn't 'index funds beat hedge funds.' It's that fees compound backwards and most active management can't overcome them over long time horizons.

- Is a 1% financial advisor fee worth it?

- It depends on what's in the bundle. Vanguard's 'Advisor's Alpha' research finds good advisors add about 3% in value per year, mostly through behavioral coaching, tax planning, estate coordination, and insurance review. The portfolio management itself is largely automated by rebalancing software. On a $500,000 portfolio at 7% returns over 30 years, a 1% fee costs roughly $900,000 in foregone growth. Whether the rest of the bundle is worth that is a question worth asking, not having decided for you.

- What does going self-directed mean?

- Managing your own investments without paying an advisor or robo-advisor a percentage of assets. Most self-directed investors run a small number of low-cost index funds, rebalance occasionally, and handle taxes themselves. Self-directed doesn't mean active stock-picking. In an analysis of 48,970 comments across nine investing subreddits, individual stock-picking represented about 0.3% of the dataset.

- Do self-directed investors pick individual stocks?

- Mostly not. The dominant communities (r/Bogleheads, r/financialindependence, r/fatFIRE) converge on a small number of low-cost index funds rebalanced occasionally. The active stock-picking subset (r/stocks, r/investing) makes up about 0.3% of the dataset, and even that subset typically describes itself as '90% index, 10% fun money.'

- What is the wash-sale rule and why does it matter for tax-loss harvesting?

- The wash-sale rule (US tax code section 1091) disallows a tax loss if you buy a 'substantially identical' security within 30 days of selling at a loss. The rule applies across all your accounts, including your spouse's IRA. If a wash sale lands inside a retirement account, IRS Revenue Ruling 2008-5 makes the disallowance permanent. The loss is gone, not deferred. Every major automated tax-loss-harvesting product (Wealthfront, Betterment, Schwab, Fidelity) explicitly disclaims monitoring this across accounts they don't custody.

- What's the difference between a robo-advisor and a financial advisor?

- Robo-advisors (Betterment, Wealthfront, Schwab Intelligent Portfolios, Vanguard Digital Advisor, Fidelity Go) automate portfolio management using model portfolios for a smaller fee, typically 0.25%. Human advisors do similar work plus the relationship layer (calls, meetings, coordination with your CPA) for around 1% of assets per year. Both rely on rebalancing software for the actual portfolio management. The work that justifies the higher human fee is the strategic call, not the operations.

- What's a recommended portfolio allocation for self-directed investors?

- We don't recommend, but the dominant patterns in self-directed communities are a target-date fund (a single fund that automatically adjusts the stock-to-bond ratio as you get older) or a three-fund portfolio (a US stock index, an international stock index, and a bond fund). The most-cited piece of advice in the data: pick a sensible default and move on. The difference between 60/40 and 70/30 is dwarfed by your savings rate.

- What does threshold-based rebalancing mean?

- Rebalancing your portfolio when an asset class drifts past a set threshold from its target allocation, instead of on a fixed calendar schedule. Vanguard's 2015 paper 'Best Practices for Portfolio Rebalancing' recommends a 5% absolute threshold. Daryanani's 2008 Journal of Financial Planning paper 'Opportunistic Rebalancing' recommends a 20% relative threshold. Both outperform calendar-based rebalancing on risk-adjusted return. The challenge is monitoring: traditional brokerages don't send drift alerts on accounts you self-manage, and the robo-advisors that do only see the accounts they custody.